|

|  | - ISM Services slows, but employment gauge returns to expansion.

- Fed hike bets cool after weaker payrolls and revisions.

- FOMC minutes, jobless claims and CPI guide next move.

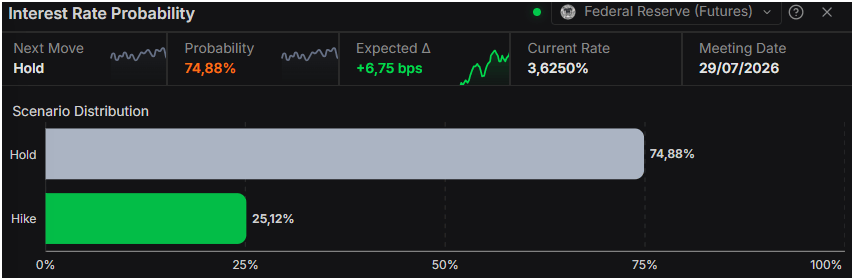

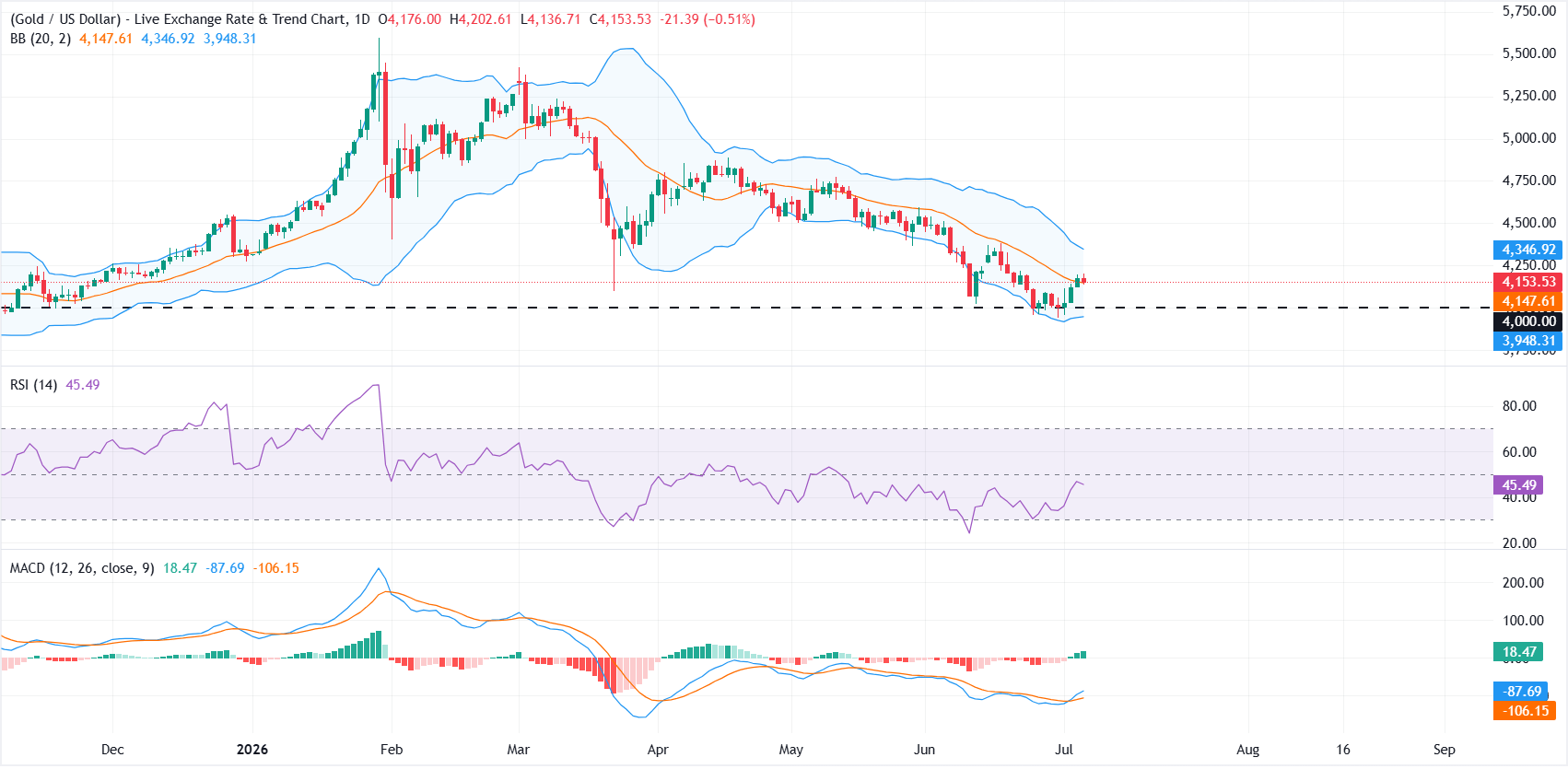

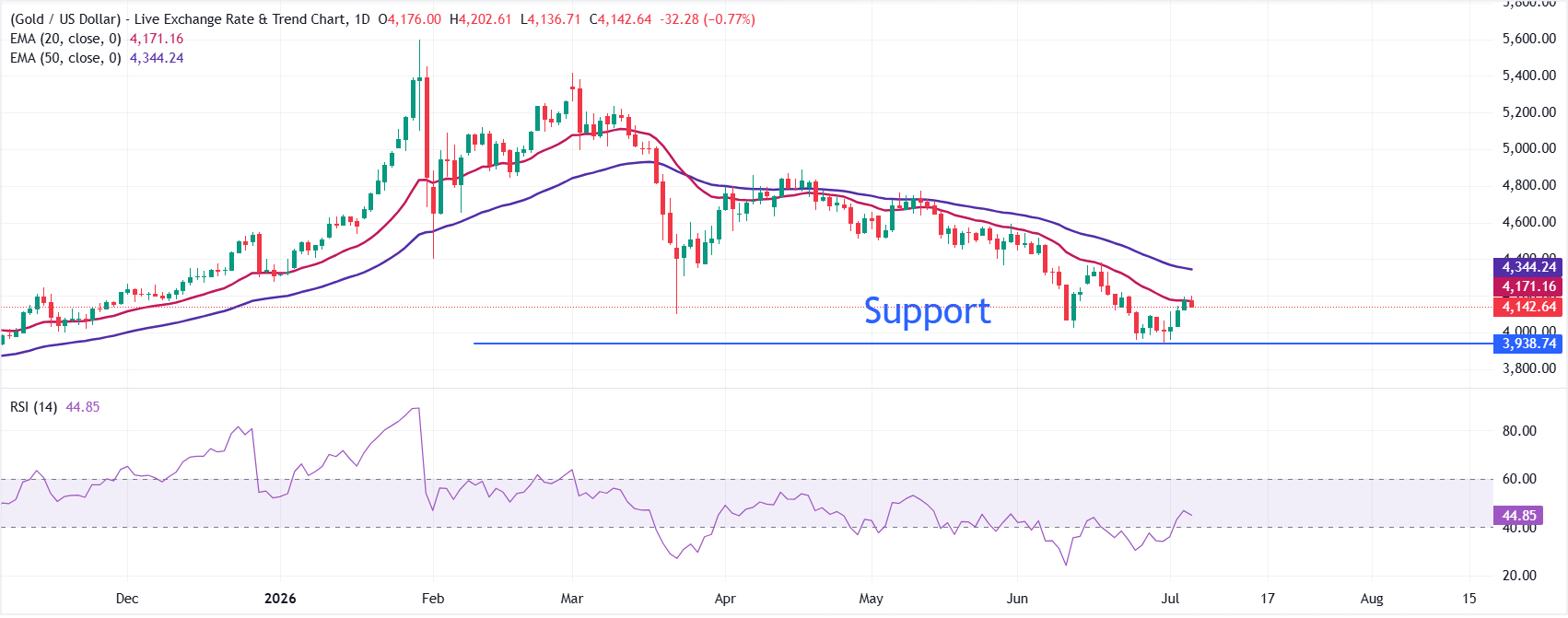

Gold (XAU/USD) price retreats by some 0.50% on Monday as the Greenback remains steady despite traders repricing a less hawkish Federal Reserve (Fed) following last Thursday’s softer-than-expected jobs report. The XAU/USD pair trades at $4,153, down 0.50%. XAU/USD retreats as steady Dollar and yields cap recoveryData from the US showed that business activity in the services sector was modestly softer than expected, with the ISM Services PMI dipping from 54.5 to 54. Even though the data indicated a slowdown, the Employment Index improved, while a measure of producer prices slowed from 71.3 to 67.7. Monday’s data outweighed June’s Nonfarm Payrolls report, which fell short of expectations, and the April and May data, revised lower, an indication of further deterioration. Traders? trimmed Fed hawkish bets. As of writing, they are expecting an 88% chance of a rate hike at the December meeting, as they priced in 22 basis points of tightening. For the July meeting, money markets expect the Fed to hold rates unchanged, with odds at 77%, according to Prime Terminal data.  Source: Prime Terminal Source: Prime TerminalBullion weighed by high US yields, strong US DollarIn the meantime, the US Dollar Index (DXY), which tracks the buck’s value against six currencies, is up 0.03% at 100.90, a headwind for the non-yielding metal. Also, US Treasury yields are steady, with the 10-year benchmark note yielding 4.451%, unchanged. Geopolitics had fallen to the background as the second round of talks between the US and Iran in Islamabad was set to start next Saturday. Remaining issues include Iran’s nuclear program, frozen assets, the Strait of Hormuz, and Lebanon. Aside from this, the US economic docket will feature the Fed’s last meeting minutes, followed by Initial Jobless Claims for the week ending July 4, as traders brace for July 14 Consumer Price Index (CPI) figures. XAU/USD technical outlook: Gold stays bearish, fails to clear $4,200Gold price downtrend is intact as long as XAU fails to clear a downtrend-resistance trendline at around $4,200-$4,225. Additionally, a 'death-cross' has formed on the daily chart, suggesting sellers have overtaken buyers and opening the door to further losses. The Relative Strength Index (RSI) is bearish, despite aiming towards its 50-neutral level. However, during the last two trading sessions, it opened the door for further downside. If XAU/USD drops below $4,200, the next support would be the psychological $4,100, before testing $4,000 and the year-to-date (YTD) low at $3,941. For a bullish reversal, Gold needs to decisively clear $4,250 before testing $4,300. Overhead lies the 50-day Simple Moving Average (SMA) at $4,391, followed by the 200-day SMA at $4,488, ahead of $4,500.  Gold daily chart Gold daily chart

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

|

|

|

| | Jul 6 2026 6:43PM EST |

|

|

| | - US Dollar trims intraday gains as traders reassess the Fed's monetary policy outlook.

- Weaker-than-expected US jobs data and easing Oil prices temper expectations of a near-term Fed rate hike.

- Traders look to FOMC minutes for fresh guidance on interest rates.

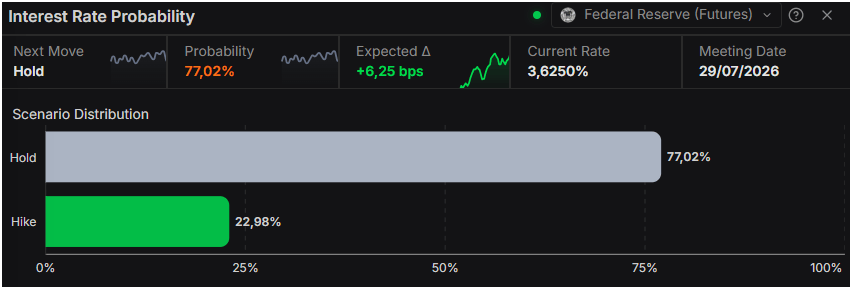

The US Dollar Index (DXY) trims its gains on Monday after opening the week on a firmer note, as traders await greater clarity on the Federal Reserve's (Fed) interest rate path before placing fresh directional bets. At the time of writing, the index, which tracks the US Dollar against a basket of six major currencies, is trading around 100.92 after easing from an intraday high of 101.14. The Fed is unlikely to raise interest rates anytime soon after Thursday's weaker-than-expected US Nonfarm Payrolls (NFP) report. At the same time, Oil prices have fully unwound their US-Iran war-driven rally as shipping through the Strait of Hormuz continues to improve following last month's interim peace agreement between the United States and Iran. Lower Oil prices have eased inflation risks, suggesting the Fed may not need to tighten monetary policy as aggressively as markets had previously feared. Even so, with inflation still running above the Fed's 2% target, policymakers remain committed to bringing inflation back to target, suggesting monetary policy is likely to remain restrictive for the time being. According to the CME FedWatch Tool, traders are pricing in a 77% probability that the Fed will keep interest rates unchanged at this month's meeting, while the probability of a rate hike at the September meeting has fallen to 56% from 63% before the US jobs report was released. Meanwhile, the United States and Iran have yet to reach a final agreement. Key sticking points include the future management of the Strait of Hormuz, the release of frozen Iranian assets, sanctions relief, and Tehran's commitments regarding its nuclear program. With geopolitical risks lingering and traders still pricing in at least one Fed rate hike this year, further downside in the US Dollar is likely to remain limited. On the data front, the ISM Services Purchasing Managers Index (PMI) came in at 54.0 in June, in line with market expectations. Although the reading eased from 54.5 in May, it marked the 23rd consecutive month of expansion. The US economic calendar is relatively light this week, with the ADP Employment Change report due on Tuesday and weekly Initial Jobless Claims on Thursday. Investors will also closely watch the Federal Open Market Committee (FOMC) meeting minutes on Wednesday for fresh clues on the Fed's monetary policy outlook.

Fed FAQs

Monetary policy in the US is shaped by the Federal Reserve (Fed). The Fed has two mandates: to achieve price stability and foster full employment. Its primary tool to achieve these goals is by adjusting interest rates.

When prices are rising too quickly and inflation is above the Fed’s 2% target, it raises interest rates, increasing borrowing costs throughout the economy. This results in a stronger US Dollar (USD) as it makes the US a more attractive place for international investors to park their money.

When inflation falls below 2% or the Unemployment Rate is too high, the Fed may lower interest rates to encourage borrowing, which weighs on the Greenback.

The Federal Reserve (Fed) holds eight policy meetings a year, where the Federal Open Market Committee (FOMC) assesses economic conditions and makes monetary policy decisions.

The FOMC is attended by twelve Fed officials – the seven members of the Board of Governors, the president of the Federal Reserve Bank of New York, and four of the remaining eleven regional Reserve Bank presidents, who serve one-year terms on a rotating basis.

In extreme situations, the Federal Reserve may resort to a policy named Quantitative Easing (QE). QE is the process by which the Fed substantially increases the flow of credit in a stuck financial system.

It is a non-standard policy measure used during crises or when inflation is extremely low. It was the Fed’s weapon of choice during the Great Financial Crisis in 2008. It involves the Fed printing more Dollars and using them to buy high grade bonds from financial institutions. QE usually weakens the US Dollar.

Quantitative tightening (QT) is the reverse process of QE, whereby the Federal Reserve stops buying bonds from financial institutions and does not reinvest the principal from the bonds it holds maturing, to purchase new bonds. It is usually positive for the value of the US Dollar.

|

|

|

| | Jul 6 2026 6:12PM EST |

|

|

| | - WTI has round-tripped the entire war premium and now sits just above its February base.

- OPEC+ lifted quotas again for August while actual Gulf output is still catching up.

- The Brent curve's slip into contango frames Wednesday's EIA inventory data as the week's main test.

West Texas Intermediate (WTI) has spent three weeks handing back what the war spent three months building, and the tape now reads as though February never ended. The US benchmark drifts near $68.50 while Brent hovers close to $72.00, both a couple of dollars above their pre-war bases and nearly 40% below the March extremes. The candles have been shrinking for a week and the ranges with them, which tells you the momentum did not fade so much as leave with the risk premium. The June 17 interim agreement between Washington and Tehran reopened the Strait of Hormuz to normal traffic, the fear trade was carried out of the building, and what remains is a market forced to price ordinary supply and demand for the first time this year. It does not appear thrilled by the exercise. The differential says the war trade is closedBrent's premium over WTI has settled near $3.50, which is plain freight-and-quality territory rather than anything resembling a risk premium. Seaborne barrels carried the fear through the war, and that gap has now compressed back to the boring arithmetic of pipelines versus tankers. Nobody is paying extra for Brent's postcode anymore, and the differential is the cleanest single gauge that the geopolitical bid has been fully extracted. Everyone is selling into the reunionThe Organization of the Petroleum Exporting Countries (OPEC) and its allies, collectively OPEC+, agreed on Sunday to add another 188K barrels per day (bpd) to August quotas, the latest step in restoring 940K bpd of paper supply since the war began. Actual output still lags the paperwork, with the biggest Gulf producers having lost around 6 million bpd at the worst of the closure, though flows have been recovering since the June agreement. The United Arab Emirates has meanwhile walked away from the quota system altogether, Washington is still working through a 172 million barrel release from the Strategic Petroleum Reserve (SPR) agreed during the war, and US production set a record near 14 million bpd in May. The curve said the quiet partThe Brent futures curve tipped into contango last week for the first time this year, with the six-month spread near minus 56 cents; when the market pays you to store barrels, it is telling you it has too many of them. OPEC's own monthly report has trimmed 2026 demand growth in back-to-back months, to under 1 million bpd, so the supply wave is arriving into a shrinking demand forecast. Strategists have begun sketching Brent into the 60s by year-end, and for once the futures market is not arguing with them. Wednesday brings the receiptsWeekly inventory data from the Energy Information Administration (EIA) lands Wednesday at 14:30 GMT, the first clean read on stockpiles since Hormuz traffic began normalizing, after industry figures Tuesday evening. Minutes from the June Federal Open Market Committee (FOMC) meeting arrive the same day at 18:00 GMT; a hawkish Federal Reserve (Fed) keeps the Dollar bid, and Dollar-priced barrels do not enjoy that. OPEC+ ministers reconvene on August 2, where a compensation-hungry Iraq is already agitating for a bigger quota. Levels to watchResistance: WTI's first hurdle is the $70.00 handle, with the June breakdown shelf near $72.00 behind it; Brent faces the same test at $74.00. Reclaiming those levels on a daily close is the minimum before anyone argues the flush is finished. Support: Initial demand sits close to $67.50 for WTI and around $71.00 for Brent, the floors of the past week's drift. Below there, $65.00 is the only round figure of note before the February bases near $62.00 for WTI and $66.50 for Brent, where this entire journey started. Bias: Bearish. The Stochastic Relative Strength Index (Stoch RSI) has been pinned near its floor for two weeks while price keeps leaking, and oversold in a downtrend is a description, not a buy signal. With quotas rising, the reserve draining, and the curve paying for storage, rallies toward $70.00 are for selling; only a daily close back above $72.00 changes the conversation, while a break of $67.50 puts the February base on the table.

WTI daily chart Brent daily chart

WTI Oil FAQs

WTI Oil is a type of Crude Oil sold on international markets. The WTI stands for West Texas Intermediate, one of three major types including Brent and Dubai Crude. WTI is also referred to as “light” and “sweet” because of its relatively low gravity and sulfur content respectively. It is considered a high quality Oil that is easily refined. It is sourced in the United States and distributed via the Cushing hub, which is considered “The Pipeline Crossroads of the World”. It is a benchmark for the Oil market and WTI price is frequently quoted in the media.

Like all assets, supply and demand are the key drivers of WTI Oil price. As such, global growth can be a driver of increased demand and vice versa for weak global growth. Political instability, wars, and sanctions can disrupt supply and impact prices. The decisions of OPEC, a group of major Oil-producing countries, is another key driver of price. The value of the US Dollar influences the price of WTI Crude Oil, since Oil is predominantly traded in US Dollars, thus a weaker US Dollar can make Oil more affordable and vice versa.

The weekly Oil inventory reports published by the American Petroleum Institute (API) and the Energy Information Agency (EIA) impact the price of WTI Oil. Changes in inventories reflect fluctuating supply and demand. If the data shows a drop in inventories it can indicate increased demand, pushing up Oil price. Higher inventories can reflect increased supply, pushing down prices. API’s report is published every Tuesday and EIA’s the day after. Their results are usually similar, falling within 1% of each other 75% of the time. The EIA data is considered more reliable, since it is a government agency.

OPEC (Organization of the Petroleum Exporting Countries) is a group of 12 Oil-producing nations who collectively decide production quotas for member countries at twice-yearly meetings. Their decisions often impact WTI Oil prices. When OPEC decides to lower quotas, it can tighten supply, pushing up Oil prices. When OPEC increases production, it has the opposite effect. OPEC+ refers to an expanded group that includes ten extra non-OPEC members, the most notable of which is Russia.

|

|

|

| | Jul 6 2026 6:08PM EST |

|

|

| | Rabobank’s FX Strategy team discusses the New Zealand Dollar (NZD) ahead of the July 8 Reserve Bank of New Zealand (RBNZ) meeting, where consensus and the bank expect a 25 bp hike to 2.5%. They note mixed views from the NZ (New Zealand) shadow board, moderating inflation as Oil falls, and a fragile domestic recovery. With nearly four hikes priced, Rabobank sees limited NZD upside and expects choppy NZD/USD ranges. RBNZ path, inflation and NZD pricing"In line with Rabobank’s view, the consensus of the Bloomberg survey points to a 25 bp rate hike, which would take the main policy rate to 2.5%. Forecasters, however, are not unanimous." "This news has clearly fanned some doubts in the market about the resolve to the RBNZ to tighten policy and has consequently weighed on the NZD. Today the NZD is positioned second to last on the G10 one day performance table, just above the JPY." "In view of the inflationary impact of this year’s closure of the Strait of Hormuz, RBNZ Governor Breman stated after the last RBNZ policy meeting in May that the central bank expects to “increase interest rates this year, to help keep a lid on inflation”. That said, oil prices have come down substantially in the wake of the June 17 signing of the MoU by the US and Iran to levels last seen just before the start of the war." "Currently, market implied interest rates suggest scope for almost four 25 bps rate hikes from the RBNZ over the next year to around 3.18%, from 2.25% currently. This is not so dissimilar to the forecasts from the NZ shadow Board, whose views are centred around rates reaching 3-3.25% over the next year." "With so much tightening already in the price, we don’t see much scope for the NZD to improve its position on the G10 performance table this year. Indeed, any sign that the RBNZ is backing down on its hawkish tone, could leave the NZD vulnerable." (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 5:57PM EST |

|

|

| | - DJIA set a fresh record high at Monday's opening bell and handed most of it back within the hour.

- The index lagged the S&P 500 and Nasdaq as chip stocks rebounded and last week's rotation ran in reverse.

- FOMC Minutes on Wednesday will show how seriously the committee is weighing a hike.

The Dow Jones Industrial Average (DJIA) finally crossed 53,000 on Monday, spiking to a record just above the handle in the opening minutes and holding it for roughly the length of the ceremony that produced it. President Trump rang the opening bell from the Oval Office in a first-of-its-kind joint event with both major exchanges. The index celebrated by tagging fresh all-time highs, and sellers removed close to 400 points inside half an hour. By early afternoon in New York the Dow sat flat near 52,900 while the S&P 500 added 0.7% and the Nasdaq rose 1.1%. The fade and the lag share one explanation: Monday was a technology session, and the Dow's march into record territory was never a technology story. Leadership on loanThe index climbed nearly 2% last week while the benchmark semiconductor fund shed more than 3% for its second straight losing week, as money rotated out of the chip trade into nearly everything else. On Monday the flow reversed, with chips bouncing roughly 3% on an expanded Broadcom supply deal with Apple, leaving the Dow holding a record it lacked the energy to extend. Strategists frame the second half as a tug-of-war between the artificial intelligence trade and the broader market. The Dow sits on the broader-market side of that argument, which makes Monday's record both real and conditional. Records with a hawkish soundtrackThe genuinely strange part of this rally is that it is happening while the market debates whether the next move from the Federal Reserve (Fed) is a hike, not a cut. Thursday's June Nonfarm Payrolls (NFP) report printed 57K against expectations above 100K, paring the hike chatter and letting stagflation worries fade into the long weekend. Monday's Institute for Supply Management (ISM) Services Purchasing Managers Index (PMI) pushed back: the headline matched consensus at 54, but the employment gauge returned to expansion at 51.2 after months of contraction, and prices paid eased to 67.7, still miles above the growth threshold. A Fed governor's afternoon remarks leaned firmly hawkish and the tape barely blinked. Rate markets still assign roughly three-in-four odds to a hold at this month's meeting, with the residual risk tilted toward tightening rather than relief. Housekeeping among the componentsMicrosoft, one of the index's heavyweights, slipped more than 1% after announcing 4.8K job cuts, about 2% of its workforce, with the Xbox unit absorbing an outsized share. Management framed the reductions as adapting to the artificial intelligence era, a polite way of saying the spending has to come from somewhere. Fellow component IBM went the other way as analysts lifted price expectations into its results later this month, a reminder that earnings will soon judge whether this record ages well. Wednesday is the only date that countsThe calendar stays second-tier until Minutes from the June Federal Open Market Committee (FOMC) meeting land at 18:00 GMT on Wednesday. The committee held at 3.75% last month with an unmistakably hawkish lean, and updated projections showed a visible bloc open to tightening again this year; the Minutes will reveal how broad that appetite runs. Around it, a private payrolls update arrives Tuesday at 12:15 GMT, weekly jobless claims follow Thursday at 12:30 GMT with consensus near 220K against 215K prior, and the New York Fed president speaks later that day. Levels to watchResistance: The 53,000 handle is the number that matters, with Monday's record just above it near 53,050. Acceptance above the handle on a daily close turns the milestone from a headline into a floor. Support: Initial demand rests around 52,750, the shelf that absorbed the morning washout, with Monday's spike low close to 52,650 beneath it and the round 52,500 area below that. Bias: Bullish. The record fade was a rotation story rather than a rejection; buyers repaired most of a 400-point flush within two hours, and the uptrend off the April base near 45,000 is not in question. A hawkish shock in Wednesday's Minutes is the one item with the weight to change that; absent it, the path of least resistance still runs through 53,000.

Dow Jones daily chart

Dow Jones FAQs

The Dow Jones Industrial Average, one of the oldest stock market indices in the world, is compiled of the 30 most traded stocks in the US. The index is price-weighted rather than weighted by capitalization. It is calculated by summing the prices of the constituent stocks and dividing them by a factor, currently 0.152. The index was founded by Charles Dow, who also founded the Wall Street Journal. In later years it has been criticized for not being broadly representative enough because it only tracks 30 conglomerates, unlike broader indices such as the S&P 500.

Many different factors drive the Dow Jones Industrial Average (DJIA). The aggregate performance of the component companies revealed in quarterly company earnings reports is the main one. US and global macroeconomic data also contributes as it impacts on investor sentiment. The level of interest rates, set by the Federal Reserve (Fed), also influences the DJIA as it affects the cost of credit, on which many corporations are heavily reliant. Therefore, inflation can be a major driver as well as other metrics which impact the Fed decisions.

Dow Theory is a method for identifying the primary trend of the stock market developed by Charles Dow. A key step is to compare the direction of the Dow Jones Industrial Average (DJIA) and the Dow Jones Transportation Average (DJTA) and only follow trends where both are moving in the same direction. Volume is a confirmatory criteria. The theory uses elements of peak and trough analysis. Dow’s theory posits three trend phases: accumulation, when smart money starts buying or selling; public participation, when the wider public joins in; and distribution, when the smart money exits.

There are a number of ways to trade the DJIA. One is to use ETFs which allow investors to trade the DJIA as a single security, rather than having to buy shares in all 30 constituent companies. A leading example is the SPDR Dow Jones Industrial Average ETF (DIA). DJIA futures contracts enable traders to speculate on the future value of the index and Options provide the right, but not the obligation, to buy or sell the index at a predetermined price in the future. Mutual funds enable investors to buy a share of a diversified portfolio of DJIA stocks thus providing exposure to the overall index.

|

|

|

| | Jul 6 2026 5:51PM EST |

|

|

| | - The Swiss Franc weakens against the US Dollar as the Greenback benefits from renewed demand.

- The ISM Services PMI meets expectations in June, while price pressures ease and employment improves.

- Investors digest an unexpected rise in the Swiss Unemployment Rate ahead of the Fed Minutes on Wednesday.

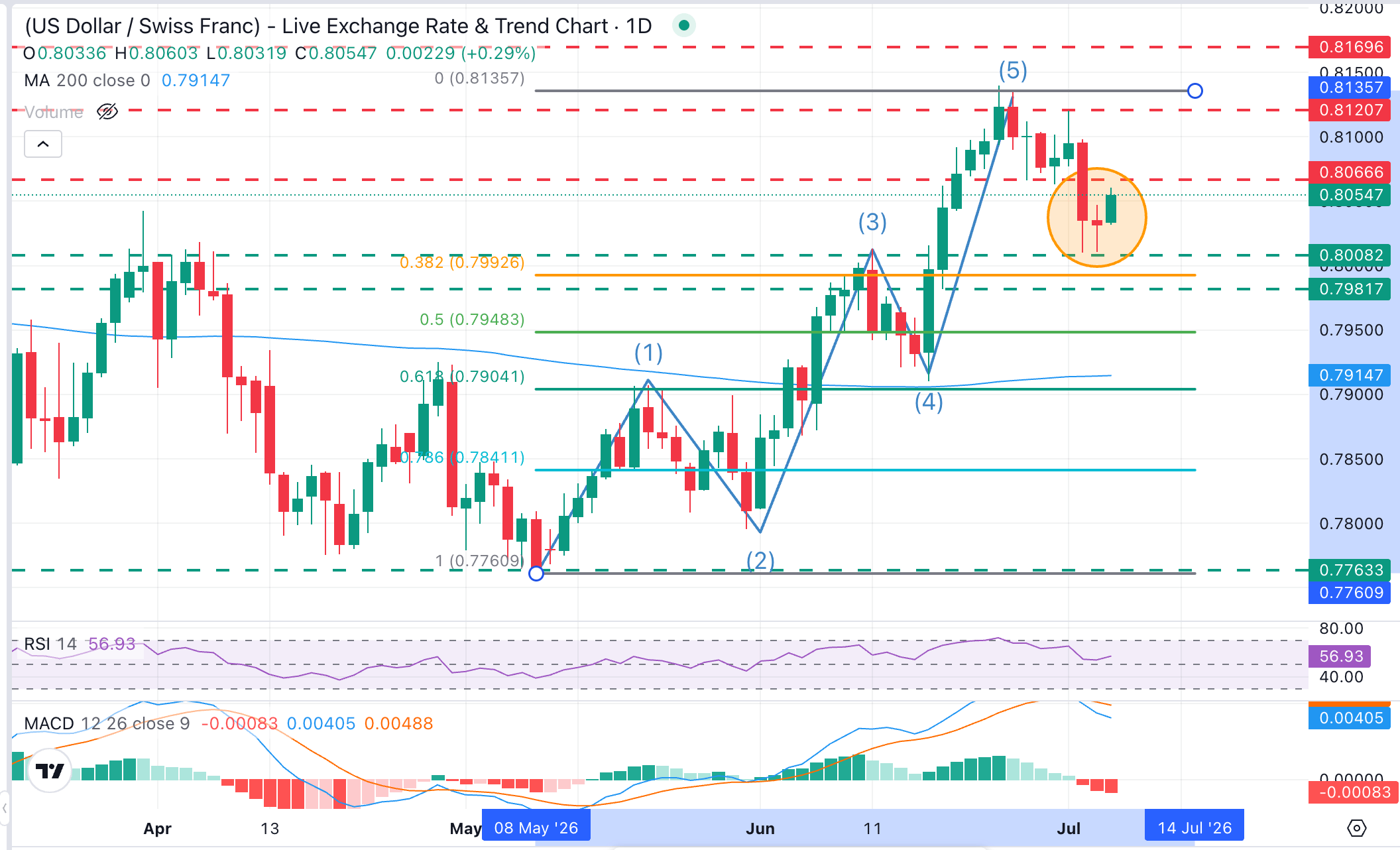

USD/CHF gains 0.37% on Monday, trading around 0.8060 at the time of writing, as the US Dollar (USD) rebounds despite slightly softer expectations for further monetary tightening by the Federal Reserve (Fed). The Greenback's recovery comes as investors reassess the monetary policy outlook following last week's weaker-than-expected United States (US) Nonfarm Payrolls (NFP) report. Despite signs of a cooling labor market, the US Dollar is benefiting from renewed demand, also supported by persistent geopolitical tensions in the Middle East, particularly around the Strait of Hormuz. According to the CME FedWatch tool, markets continue to price in a scenario of additional Fed interest rate hikes by the end of the year, with a 76.9% chance. Investors are now awaiting the release of the Federal Open Market Committee (FOMC) Minutes from the June policy meeting on Wednesday for further guidance on the outlook for monetary policy. Fresh US data released on Monday showed that the ISM Services Purchasing Managers Index (PMI) eased slightly to 54 in June from 54.5 in May, matching market expectations. The survey indicated softer New Orders and lower Prices Paid, while the Employment Index improved. In Switzerland, the Unemployment Rate unexpectedly rose to 3.1% in June, compared with 3% in May and the market expectation of 3%. The slight deterioration in labor market conditions weighed on the Swiss Franc (CHF) at the start of the week, adding further support to the USD/CHF pair.

Swiss Franc Price Today

The table below shows the percentage change of Swiss Franc (CHF) against listed major currencies today. Swiss Franc was the strongest against the Japanese Yen.

|

USD |

EUR |

GBP |

JPY |

CAD |

AUD |

NZD |

CHF |

| USD |

|

0.06% |

-0.16% |

0.57% |

0.13% |

-0.07% |

0.30% |

0.32% |

| EUR |

-0.06% |

|

-0.21% |

0.50% |

0.07% |

-0.11% |

0.25% |

0.26% |

| GBP |

0.16% |

0.21% |

|

0.72% |

0.26% |

0.05% |

0.47% |

0.49% |

| JPY |

-0.57% |

-0.50% |

-0.72% |

|

-0.44% |

-0.63% |

-0.28% |

-0.19% |

| CAD |

-0.13% |

-0.07% |

-0.26% |

0.44% |

|

-0.22% |

0.18% |

0.22% |

| AUD |

0.07% |

0.11% |

-0.05% |

0.63% |

0.22% |

|

0.40% |

0.43% |

| NZD |

-0.30% |

-0.25% |

-0.47% |

0.28% |

-0.18% |

-0.40% |

|

0.02% |

| CHF |

-0.32% |

-0.26% |

-0.49% |

0.19% |

-0.22% |

-0.43% |

-0.02% |

|

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Swiss Franc from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent CHF (base)/USD (quote).

|

|

|

| | Jul 6 2026 4:55PM EST |

|

|

| | - USD/JPY climbs toward 162.30 on Monday, supported by a broad-based US Dollar rally.

- Investors remain alert to the risk of intervention by Japanese authorities as the pair approaches 40-year highs.

- MUFG believes markets are still underpricing the Bank of Japan's monetary policy normalization outlook.

USD/JPY trades around 162.30 on Monday at the time of writing, up 0.58% on the day, extending its rebound after last week's pullback. The pair is moving back toward the nearly 40-year high of 162.84 reached on Wednesday, as broad US Dollar (USD) strength continues to dominate the foreign exchange market and keep pressure on the Japanese Yen (JPY). The US Dollar is benefiting from renewed demand despite last week's weaker-than-expected Nonfarm Payrolls (NFP) report. Investors are reassessing the Federal Reserve's (Fed) policy outlook, while geopolitical tensions in the Middle East, particularly surrounding the Strait of Hormuz, are also supporting safe-haven flows into the Greenback. At the same time, the wide interest rate differential between the United States (US) and Japan continues to fuel carry trades at the expense of the Japanese Yen. Although the Bank of Japan (BoJ) is gradually normalizing its monetary policy, its interest rates remain well below those of other major central banks, limiting support for the Japanese currency. The persistent weakness of the Japanese Yen is nevertheless keeping markets on alert. Japanese officials recently reiterated that they stand ready to intervene against excessive foreign exchange moves, although no action has been taken so far. Some market participants believe Tokyo could opt for an unannounced intervention to catch speculative traders off guard. Meanwhile, MUFG analysts argue that markets are still underpricing the Bank of Japan's tightening potential. According to the bank, accelerating inflation and rising Japanese government Bond yields could push the central bank to raise interest rates further in the coming months. MUFG now expects the policy rate to reach 1.5% by January 2027, with the next rate hike projected for September. At the same time, HSBC believes USD/JPY could remain in a higher trading range for an extended period as long as the US-Japan interest rate differential remains wide. However, the bank also expects Japan's Ministry of Finance to continue intervening selectively to prevent excessive depreciation of the JPY.

Japanese Yen Price Today

The table below shows the percentage change of Japanese Yen (JPY) against listed major currencies today. Japanese Yen was the strongest against the Swiss Franc.

|

USD |

EUR |

GBP |

JPY |

CAD |

AUD |

NZD |

CHF |

| USD |

|

0.08% |

-0.12% |

0.57% |

0.12% |

-0.06% |

0.35% |

0.34% |

| EUR |

-0.08% |

|

-0.19% |

0.50% |

0.06% |

-0.12% |

0.27% |

0.26% |

| GBP |

0.12% |

0.19% |

|

0.67% |

0.23% |

0.02% |

0.47% |

0.47% |

| JPY |

-0.57% |

-0.50% |

-0.67% |

|

-0.45% |

-0.63% |

-0.24% |

-0.17% |

| CAD |

-0.12% |

-0.06% |

-0.23% |

0.45% |

|

-0.21% |

0.22% |

0.25% |

| AUD |

0.06% |

0.12% |

-0.02% |

0.63% |

0.21% |

|

0.43% |

0.43% |

| NZD |

-0.35% |

-0.27% |

-0.47% |

0.24% |

-0.22% |

-0.43% |

|

-0.00% |

| CHF |

-0.34% |

-0.26% |

-0.47% |

0.17% |

-0.25% |

-0.43% |

0.00% |

|

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Japanese Yen from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent JPY (base)/USD (quote).

|

|

|

| | Jul 6 2026 4:16PM EST |

|

|

| | - Fed hike bets cool after weak payrolls and revisions.

- ISM Services eases, but employment component returns to expansion.

- Burnham chancellor uncertainty keeps Cable capped near 1.3400.

The Pound Sterling steadies during the North American session, as the week begins in a risk-off mood, as evidenced by overall US Dollar strength in the FX markets, even though soft jobs data and trimmed hawkish Fed bets for the rest of the year. At the time of writing, the GBP/USD trades at 1.3357 after reaching a daily low of 1.3328. GBP/USD steadies as Dollar demand offsets softer Fed repricingLast week's US jobs report missed estimates, while figures for April and May were downwardly revised, triggering a repricing of a less hawkish Federal Reserve. Nevertheless, the Unemployment Rate is within the 4.5% level pencilled by officials towards the end of the year. Money markets had priced in a 22 basis points of tightening for the year’s end, according to Fed funds rates futures contracts. Meanwhile, for the upcoming July meeting, there’s a 77% chance the Fed will keep rates unchanged, versus a slim 23% chance of an increase, according to Prime Terminal.  Source: Prime Terminal Source: Prime TerminalRecently, the Institute for Supply Management (ISM) revealed that the Services PMI came as expected at 54.0 but ticked lower from 54.5. Other survey measures showed that input costs eased somewhat, while the Services Employment Index improved from 47.9 to 51.2. Across the pond, the UK economic calendar was light on Monday, yet Cable is still underpinned by a slight chance of a single rate hike by the Bank of England (BoE) towards the end of the year. A month ago, money markets were pricing in at least 44 basis points of tightening, but as of writing, the swaps market is pricing in 17 basis points, implying a 70% chance of a hike. Last week, BoE Governor Andrew Bailey disregarded the chance to consider rate cuts, even though the energy shock subsided, as the US and Iran are set to begin talks by the weekend Geopolitics had taken a back seat as the second round of discussion in Islamabad would begin on July 11th. Some of the issues pending for discussion are Iran’s nuclear program, frozen assets, the Strait of Hormuz and Lebanon. In the UK, there’s uncertainty about who Andy Burnham would pick as finance minister. Newswires reported that there’s a 55% chance that Ed Miliband, a former energy minister, would be tapped as the Chancellor succeeding Rachel Reeves. Hence, the GBP/USD pair would be leaning on political uncertainty in the UK. This could pave the way for some consolidation at around current levels, at around 1.3300-1.3400, until a chancellor is picked. GBP/USD Price Forecast: Technical outlook GBP/USD daily chart GBP/USD daily chartIn the daily chart, GBP/USD trades at 1.3365, maintaining a mildly bearish bias as spot holds below the simple moving average cluster now converging around 1.3406. The pair is effectively capped by this SMA resistance and the broader downward trend-line barrier near 1.3513, even as the 14-day Relative Strength Index hovers in neutral-to-slightly positive territory around 55, suggesting only modest upside momentum that has yet to reclaim the overhanging structure. On the topside, immediate resistance emerges at the simple moving average near 1.3406, with a stronger cap defined by the descending trend line around 1.3513. On the downside, the first notable structural floor aligns with the rising support trend line drawn from prior lows around 1.3159, where a break would likely expose a deeper retracement within the broader range despite the currently subdued momentum backdrop. (The technical analysis of this story was written with the help of an AI tool. Know more.)

Pound Sterling FAQs

The Pound Sterling (GBP) is the oldest currency in the world (886 AD) and the official currency of the United Kingdom. It is the fourth most traded unit for foreign exchange (FX) in the world, accounting for 12% of all transactions, averaging $630 billion a day, according to 2022 data.

Its key trading pairs are GBP/USD, also known as ‘Cable’, which accounts for 11% of FX, GBP/JPY, or the ‘Dragon’ as it is known by traders (3%), and EUR/GBP (2%). The Pound Sterling is issued by the Bank of England (BoE).

The single most important factor influencing the value of the Pound Sterling is monetary policy decided by the Bank of England. The BoE bases its decisions on whether it has achieved its primary goal of “price stability” – a steady inflation rate of around 2%. Its primary tool for achieving this is the adjustment of interest rates.

When inflation is too high, the BoE will try to rein it in by raising interest rates, making it more expensive for people and businesses to access credit. This is generally positive for GBP, as higher interest rates make the UK a more attractive place for global investors to park their money.

When inflation falls too low it is a sign economic growth is slowing. In this scenario, the BoE will consider lowering interest rates to cheapen credit so businesses will borrow more to invest in growth-generating projects.

Data releases gauge the health of the economy and can impact the value of the Pound Sterling. Indicators such as GDP, Manufacturing and Services PMIs, and employment can all influence the direction of the GBP.

A strong economy is good for Sterling. Not only does it attract more foreign investment but it may encourage the BoE to put up interest rates, which will directly strengthen GBP. Otherwise, if economic data is weak, the Pound Sterling is likely to fall.

Another significant data release for the Pound Sterling is the Trade Balance. This indicator measures the difference between what a country earns from its exports and what it spends on imports over a given period.

If a country produces highly sought-after exports, its currency will benefit purely from the extra demand created from foreign buyers seeking to purchase these goods. Therefore, a positive net Trade Balance strengthens a currency and vice versa for a negative balance.

|

|

|

| | Jul 6 2026 3:55PM EST |

|

|

| | Scotiabank strategists Shaun Osborne and Eric Theoret note GBP/USD near 1.3338 is steady versus the US Dollar (USD) and outperforming on crosses despite weak construction Purchasing Managers' Index (PMI) data. The data calendar and Bank of England (BoE) speeches are limited, while rate expectations have stabilized and the curve has un-inverted. Markets see little change at the July and September meetings, pricing modest tightening by November and December, with spot seen in a 1.3300–1.3400 range. Pound steady in tight range"The pound is steady, entering Monday’s NA session unchanged vs. the USD while outperforming most of the G10 currencies on the crosses." "Fundamental releases have been limited to third-tier construction PMI data, disappointing with a deeply contractionary print of 38.4 – a marginal rise from the prior month’s multi-year low of 38.2." "This week’s data calendar is thin and BoE speaking engagements are sparse. BoE rate expectations stabilized over the past week or so, and have also un-inverted in a manner similar to the ECB’s. Markets are pricing little change for either of the next two (July 30, Sept 17) meetings, with 12bpts of tightening for November and 17bpts by December." "Neutral – the RSI has recovered back to the neutral threshold around 50, reflecting the recovery in spot from the mid-1.31s to the upper 1.33s. We see potential near-term resistance around 1.34, a level that roughly corresponds to both the 50 and 200 day MA’s. We look to a near-term range bound between 1.3300 and 1.3400." (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 3:51PM EST |

|

|

| | - EUR/USD retreats as the US Dollar starts the week on a firmer footing.

- Fed and ECB are expected to keep monetary policy restrictive for now.

- ISM Services PMI points to continued resilience in the US services sector.

The Euro (EUR) trades on the back foot against the US Dollar (USD) on Monday as investors return after the extended US Independence Day weekend. At the time of writing, EUR/USD is trading around 1.1421, down 0.12% on the day. Trading conditions remain relatively subdued at the start of the week as markets reassess the monetary policy outlook for both the Federal Reserve (Fed) and the European Central Bank (ECB). Lower Oil prices after last month's interim US-Iran peace deal have eased inflation concerns, reducing pressure on central banks to tighten monetary policy aggressively. Last week's weaker-than-expected US Nonfarm Payrolls (NFP) report also lowered expectations of a near-term Fed rate hike. At the same time, softer-than-expected Eurozone inflation data reduced the likelihood of another ECB rate increase this year. ING's Chris Turner said, "A September rate hike from the European Central Bank is now priced with less than a 50% probability, but it is too early for the ECB to sound the 'all-clear' on inflation, given the risk that core inflation could still edge higher over the coming months." As inflation remains above both central banks' targets, monetary policy is likely to remain restrictive until there is clearer evidence that price pressures are moving sustainably back toward the 2% target. According to the CME FedWatch Tool, traders are currently pricing in a 56% probability of a rate hike at the September meeting. As a result, the interest rate differential continues to favor the US Dollar. The Fed's policy rate currently stands at 3.50%-3.75%, compared with the ECB's 2.25% deposit rate. The US Dollar Index (DXY), which tracks the Greenback against a basket of six major currencies, is trading around 101.04, rebounding modestly from last week's low of 100.56. On the data front, the ISM Services Purchasing Managers Index (PMI) came in at 54.0 in June, matching market expectations. While the reading eased from 54.5 in May, it marked the 23rd consecutive month of expansion.

US Dollar Price Today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Japanese Yen.

|

USD |

EUR |

GBP |

JPY |

CAD |

AUD |

NZD |

CHF |

| USD |

|

0.11% |

-0.09% |

0.58% |

0.11% |

-0.06% |

0.37% |

0.35% |

| EUR |

-0.11% |

|

-0.19% |

0.48% |

-0.01% |

-0.15% |

0.26% |

0.24% |

| GBP |

0.09% |

0.19% |

|

0.65% |

0.16% |

-0.01% |

0.46% |

0.45% |

| JPY |

-0.58% |

-0.48% |

-0.65% |

|

-0.48% |

-0.63% |

-0.23% |

-0.17% |

| CAD |

-0.11% |

0.00% |

-0.16% |

0.48% |

|

-0.18% |

0.27% |

0.28% |

| AUD |

0.06% |

0.15% |

0.01% |

0.63% |

0.18% |

|

0.45% |

0.41% |

| NZD |

-0.37% |

-0.26% |

-0.46% |

0.23% |

-0.27% |

-0.45% |

|

-0.01% |

| CHF |

-0.35% |

-0.24% |

-0.45% |

0.17% |

-0.28% |

-0.41% |

0.01% |

|

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the US Dollar from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent USD (base)/JPY (quote).

|

|

|

| | Jul 6 2026 3:45PM EST |

|

|

| | European Central Bank (ECB) Executive Board member Isabel Schnabel said on Monday that the Eurozone is not back to a pre-war situation, even after the recent decline in Oil prices. Speaking at an event in Rome, Schnabel warned that the current inflation shock cannot be ignored by policymakers, as it is already creating indirect effects and could trigger second-round inflation pressures. Key takeaways:The Eurozone is not in a pre-war situation, even after the fall in oil prices.

The current shock cannot simply be looked through by the ECB.”

|

|

|

| | Jul 6 2026 3:45PM EST |

|

|

| | Federal Reserve (Fed) Governor Christopher Waller said on Monday that forward guidance can strengthen the impact of monetary policy when used properly, but warned that it can also become problematic if it limits policymakers’ flexibility. Speaking in prepared remarks for a Bank of Italy conference in Rome, Waller said forward guidance “can be a valuable tool” and has at times helped improve policymaking. Key takeaways:Forward guidance can be a valuable tool for monetary policy and may continue to be useful.

When effective, forward guidance can speed up the impact of monetary policy, as seen in late 2021.

Guidance can become a problem if it is too strong, too rigid, or limits flexibility under uncertain economic conditions.

Waller did not provide comments on the current economy or the Fed’s policy outlook.”

|

|

|

| | Jul 6 2026 3:32PM EST |

|

|

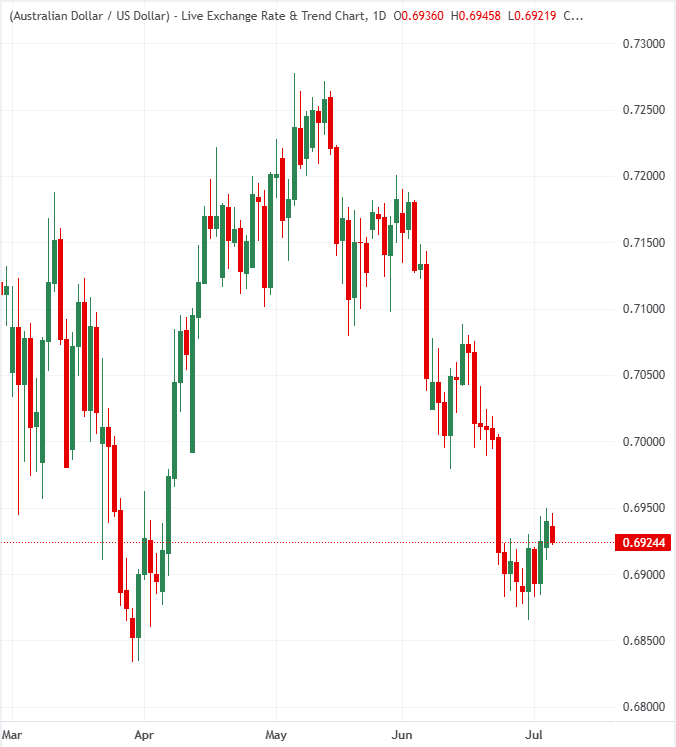

| | - AUD/USD holds near 0.6930 as softer Australian inflation limits demand for the Aussie.

- Australia’s TD-MI Inflation Gauge eased to 3.9% YoY in June from 4.4%.

- US S&P Global Services PMI slipped to 51.2, while ISM Services PMI matched expectations at 54.

AUD/USD trades with a cautious tone, sideways near the 0.6930 level on Monday after Australian inflation data showed further easing price pressures, while mixed United States (US) services figures kept the US Dollar (USD) broadly supported but without strong momentum. Australia’s TD-MI Inflation Gauge slowed to 3.9% YoY in June, down from the previous 4.4%, suggesting domestic inflation pressures are losing strength. The softer reading could reduce pressure on the Reserve Bank of Australia (RBA) to maintain a more hawkish stance, weighing on the Australian Dollar (AUD). In the United States, the S&P Global Composite Purchasing Managers Index (PMI) eased to 51.9 in June from 52.2, while the Services PMI slipped to 51.2, below expectations of 51.4 and slightly under the previous 51.3. The data pointed to slower but still positive private-sector activity, limiting aggressive USD upside. The ISM Services PMI came in at 54, matching expectations but easing from 54.5 previously. Under the surface, the Employment Index improved sharply to 51.2 from 47.9, signaling renewed hiring strength in the services sector. However, New Orders eased to 55.1 from 57.3, while Prices Paid fell to 67.7 from 71.3, suggesting that demand and cost pressures cooled.

Short-term technical analysis:On the 4-hour chart, AUD/USD trades at 0.6936. The pair holds a neutral to mildly constructive tone as it trades above the 20-period Simple Moving Average (SMA) at 0.6919 but remains capped below the 100-period SMA at 0.6962. A nearby pivot at 0.6935 is being probed, while the Relative Strength Index (RSI) around 57 hints at steady but not overextended bullish momentum within this short-term consolidation. On the topside, initial resistance is seen at 0.6944, with the higher 100-period SMA at 0.6962 forming the next cap and defining a broader supply zone. On the downside, the immediate pivot support sits just below at 0.6935, followed by clustered horizontal floors at 0.6929 and 0.6924, which together underpin the pair and would need to give way to revive a deeper bearish phase. (The technical analysis of this story was written with the help of an AI tool. Know more.) |

|

|

| | Jul 6 2026 3:14PM EST |

|

|

| | United Overseas Bank’s (UOB) Quek Ser Leang indicates USD/CNH has seen a slight softening in momentum but remains confined to a narrow intraday band of 6.7800–6.7930. Over the next 1–3 weeks, the bank expects range trading between 6.7750 and 6.8080 as earlier Dollar strength has faded. On a multi-week view, a sustained recovery requires a break above the 21-week EMA at 6.8430. Offshore Yuan pair stays range bound"24-HOUR VIEW: We highlighted last Friday that “there has been a slight increase in downward momentum, but this is likely to lead to USD trading in a lower range of 6.7820/6.7940 rather than a sustained decline.” We were not wrong, although USD traded within a narrower range than expected (6.7811/6.7896). There has been no further increase in downward momentum, and we continue to expect USD to trade in a range, most likely between 6.7800 and 6.7930." "1-3 WEEKS VIEW: Last Wednesday (01 Jul, spot at 6.7920), we highlighted that the recent USD “strength has come to an end.” We also highlighted that USD “is likely to trade in a range between 6.7750 and 6.8080.” Although USD has been edging lower since then, there has been no clear increase in downward momentum. In other words, there is no change in our view" (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 3:03PM EST |

|

|

| | BNY’s Geoff Yu notes that crowded exposure to Latin American (LatAm) bonds is unwinding as higher U.S. yields drive a domestic repricing of real-rate risks. The bank sees flows rotating toward regional equities and maintains a constructive tactical view on Latin American carry. Peru, Mexico and United States-Mexico-Canada Agreement (USMCA)-related developments are highlighted as key policy and political drivers for regional assets. Bond outflows, equity and carry appeal"Our longstanding concern about over-crowded exposure to Latin American bonds is beginning to materialize. End-June flows marked the first time in two months that the monthly smoothed flow score turned negative." "Combined with stretched FX positioning, higher U.S. yields leave Latin America's yield-sensitive bond markets vulnerable to further adjustment." "That does not imply broad capital outflows from the region. Instead, our data point to rotation rather than retrenchment, with equity flows approaching net purchase territory after a particularly weak May." "Given the structurally lower FX hedge ratios associated with equity inflows, this rotation does not undermine our constructive tactical view on Latin American carry, where regional currencies remain our preferred expression." "Forward look: Peru’s central bank is expected to leave rates unchanged this week, although inflation remains above target and a hawkish bias is likely until the Fed signals a clearer shift in direction." (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 2:48PM EST |

|

|

| | - Silver snaps a four-day winning streak as a firmer US Dollar caps gains.

- Weaker-than-expected US jobs data eases expectations of a near-term Fed rate hike, supporting Silver's near-term outlook.

- The technical backdrop remains bearish as the metal remains capped below major moving averages.

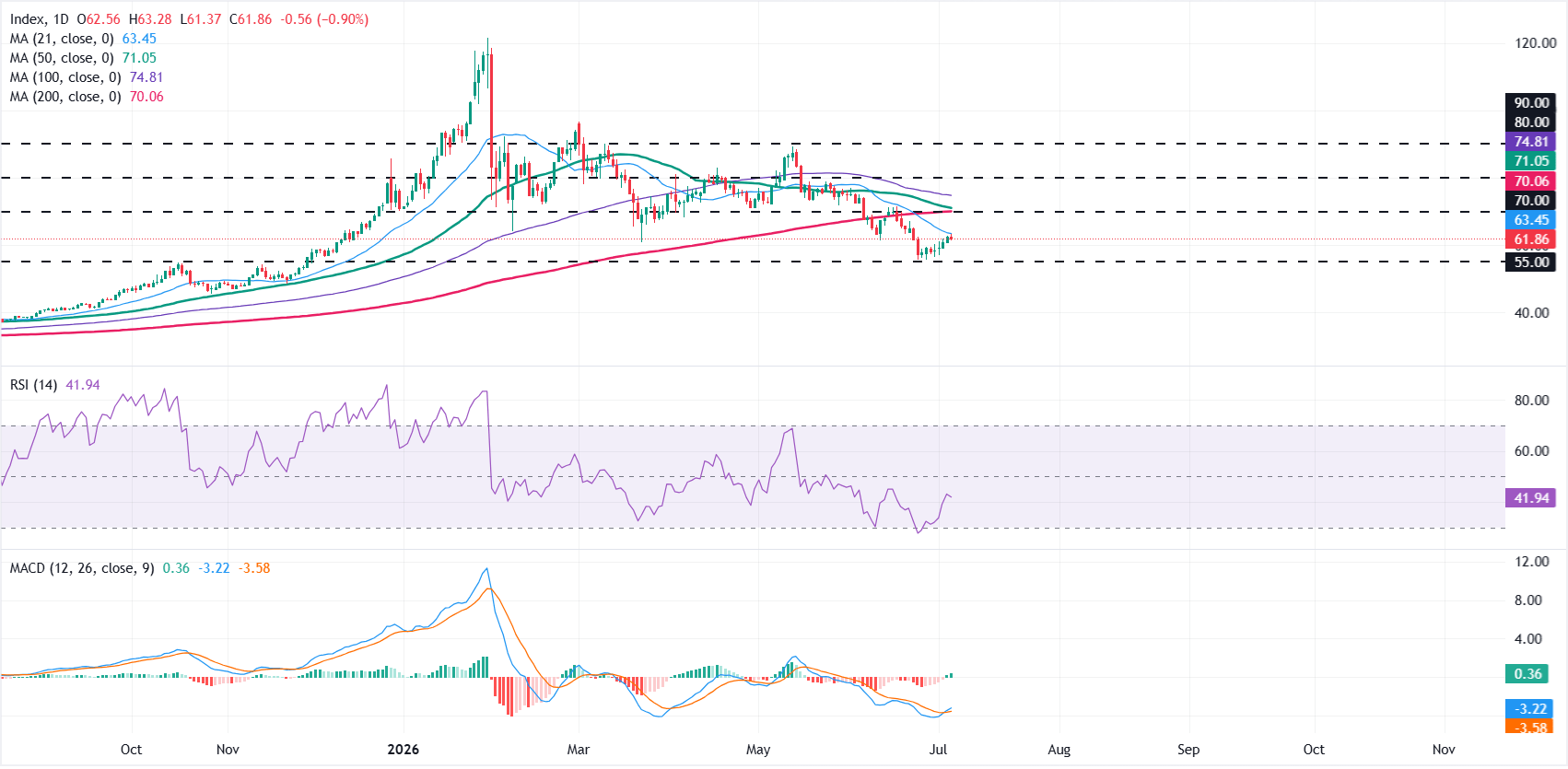

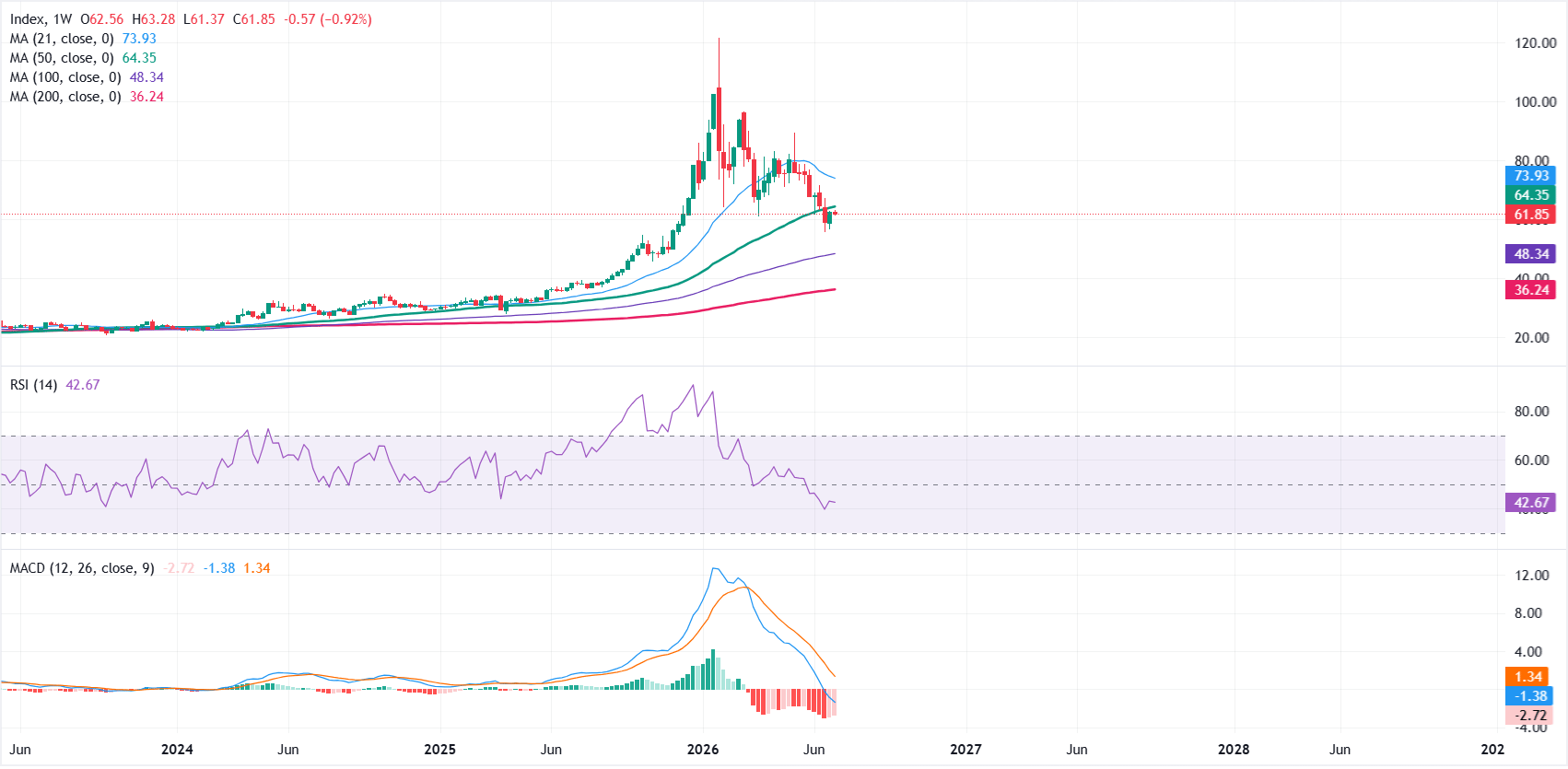

Silver (XAG/USD) pauses a four-day winning streak on Monday as buyers take a breather following last week's 5.55% rally. A firmer US Dollar (USD) is also capping the precious metal's upside. At the time of writing, XAG/USD is trading around $61.75, easing from its intraday high of $63.28, the highest level since June 23. The US Dollar Index (DXY), which tracks the Greenback's value against a basket of six major currencies is trading around 100.12, up 0.22% on the day. Despite Monday's modest pullback, Silver's near-term outlook remains supported by easing expectations of a near-term Federal Reserve (Fed) interest rate hike following weaker-than-expected US Nonfarm Payrolls (NFP) data released on Thursday. However, the technical picture tells a different story, as Silver remains capped below both its short- and long-term moving averages. Technical analysis: In the daily chart, XAG/USD remains in a bearish near-term bias as price holds below the 21-day Simple Moving Average (SMA) at $63.45 and the broader 200-day SMA at $70.06, underscoring a market that is still capped by medium- and long-term trend resistance. The Relative Strength Index (RSI) has recovered from oversold levels but remains around 42, while the Moving Average Convergence Divergence (MACD) has turned slightly positive, suggesting the rebound may be temporary within the broader downtrend. On the topside, initial resistance emerges at the 21-day SMA near $63.45, with a more meaningful barrier at the $70 horizontal level, reinforced by the 200-day SMA at $70.06 and the 50-day SMA at $71.05 clustering just above. Further up, the 100-day SMA around $74.81 precedes additional caps at $80 and $90. On the downside, the next notable support is the horizontal floor near $55.00, where buyers could attempt to stabilize the decline if bearish pressure resumes.  In the weekly chart, XAG/USD holds a clear bullish structural bias as price remains well above the 100-week and 200-week Simple Moving Averages (SMAs) at roughly $48.34 and $36.24, respectively, underscoring a firmly supported medium-term uptrend. Momentum, however, looks subdued: the RSI hovers near 43, while the Moving Average Convergence Divergence (MACD) remains negative, which together hint that upside traction is waning despite the broader bullish backdrop. On the topside, initial resistance emerges at the 50-week SMA near $64.35, with a stronger barrier higher up at the 21-week SMA around $73.93, levels that would need to be reclaimed to revive a more aggressive bullish phase. On the downside, immediate support is seen at the 100-week SMA at $48.34, ahead of the deeper structural floor at the 200-week SMA near $36.24, where the broader bullish trend would be expected to attract buyers on a more pronounced correction. (The technical analysis of this story was written with the help of an AI tool. Know more.)

Silver FAQs

Silver is a precious metal highly traded among investors. It has been historically used as a store of value and a medium of exchange. Although less popular than Gold, traders may turn to Silver to diversify their investment portfolio, for its intrinsic value or as a potential hedge during high-inflation periods. Investors can buy physical Silver, in coins or in bars, or trade it through vehicles such as Exchange Traded Funds, which track its price on international markets.

Silver prices can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can make Silver price escalate due to its safe-haven status, although to a lesser extent than Gold's. As a yieldless asset, Silver tends to rise with lower interest rates. Its moves also depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAG/USD). A strong Dollar tends to keep the price of Silver at bay, whereas a weaker Dollar is likely to propel prices up. Other factors such as investment demand, mining supply – Silver is much more abundant than Gold – and recycling rates can also affect prices.

Silver is widely used in industry, particularly in sectors such as electronics or solar energy, as it has one of the highest electric conductivity of all metals – more than Copper and Gold. A surge in demand can increase prices, while a decline tends to lower them. Dynamics in the US, Chinese and Indian economies can also contribute to price swings: for the US and particularly China, their big industrial sectors use Silver in various processes; in India, consumers’ demand for the precious metal for jewellery also plays a key role in setting prices.

Silver prices tend to follow Gold's moves. When Gold prices rise, Silver typically follows suit, as their status as safe-haven assets is similar. The Gold/Silver ratio, which shows the number of ounces of Silver needed to equal the value of one ounce of Gold, may help to determine the relative valuation between both metals. Some investors may consider a high ratio as an indicator that Silver is undervalued, or Gold is overvalued. On the contrary, a low ratio might suggest that Gold is undervalued relative to Silver.

|

|

|

| | Jul 6 2026 2:44PM EST |

|

|

| | - The Canadian Dollar remains under pressure against the US Dollar despite support from rising Oil prices.

- Markets continue to favor the Greenback as investors expect multiple Federal Reserve rate hikes this year.

- Scotiabank says the Canadian Dollar remains weighed down by trade uncertainty, even as its undervaluation has narrowed.

USD/CAD extends its advance for a second consecutive day and trades around 1.4230 at the time of writing on Monday, up 0.20% on the day. Despite higher Oil prices, which would normally support the commodity-linked Canadian Dollar (CAD), the Loonie remains under pressure against the US Dollar (USD) as investors continue to favor the Greenback. Shipping traffic through the Strait of Hormuz is gradually returning to normal after disruptions over the weekend, while the Organization of the Petroleum Exporting Countries and its allies (OPEC+) approved a 188K-barrel-per-day production increase for next month, led by Saudi Arabia and Russia. The decision is viewed as a sign of confidence in regional stability, although it has also revived concerns about a potential global supply surplus. The US Dollar continues to strengthen as markets expect further monetary tightening from the Federal Reserve (Fed). According to the CME FedWatch tool, investors are pricing in a 76.9% chance of additional interest rate hikes by the end of the year. Market participants are now awaiting the release of the Fed's June meeting minutes on Wednesday for further guidance on the outlook for monetary policy. Meanwhile, the US ISM Services Purchasing Managers Index (PMI) eased slightly to 54 in June from 54.5 previously, matching market expectations. The survey showed weaker New Orders and softer Prices Paid, while the Employment Index improved, suggesting the US services sector continues to expand at a solid pace. According to Scotiabank, the Canadian Dollar retains a soft bias despite narrower short-term yield spreads between Canada and the United States (USD). The bank notes that confirmation of the non-renewal of the United States-Mexico-Canada Agreement (USMCA) extends trade uncertainty for Canadian exporters. Analysts also expect the Bank of Canada's (BoC) Business Outlook Survey to reflect this cautious environment. While the Canadian Dollar remains fundamentally undervalued, Scotiabank believes that this undervaluation has narrowed steadily, limiting the currency's upside potential in the near term.

Canadian Dollar Price Today

The table below shows the percentage change of Canadian Dollar (CAD) against listed major currencies today. Canadian Dollar was the strongest against the Japanese Yen.

|

USD |

EUR |

GBP |

JPY |

CAD |

AUD |

NZD |

CHF |

| USD |

|

0.17% |

-0.01% |

0.60% |

0.24% |

0.08% |

0.49% |

0.46% |

| EUR |

-0.17% |

|

-0.18% |

0.43% |

0.07% |

-0.07% |

0.33% |

0.27% |

| GBP |

0.01% |

0.18% |

|

0.61% |

0.23% |

0.06% |

0.52% |

0.48% |

| JPY |

-0.60% |

-0.43% |

-0.61% |

|

-0.38% |

-0.52% |

-0.14% |

-0.10% |

| CAD |

-0.24% |

-0.07% |

-0.23% |

0.38% |

|

-0.17% |

0.26% |

0.24% |

| AUD |

-0.08% |

0.07% |

-0.06% |

0.52% |

0.17% |

|

0.43% |

0.40% |

| NZD |

-0.49% |

-0.33% |

-0.52% |

0.14% |

-0.26% |

-0.43% |

|

-0.04% |

| CHF |

-0.46% |

-0.27% |

-0.48% |

0.10% |

-0.24% |

-0.40% |

0.04% |

|

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Canadian Dollar from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent CAD (base)/USD (quote).

|

|

|

| | Jul 6 2026 2:42PM EST |

|

|

| | Scotiabank strategists Shaun Osborne and Eric Theoret note EUR/USD around 1.1418 trading softer against the US Dollar, though mid-pack within G10. Euro area Producer Price Index (PPI) and retail sales were in line with expectations, while German factory orders surprised higher. Short-term rates have stabilized and the curve normalized, with markets expecting no European Central Bank (ECB) move on July 23 and a 50% chance of a September hike. Euro soft as curve normalizes"The EUR is soft, down 0.2% vs. the USD and a mid-performer among the G10 in an environment of broad-based USD strength." "The short-term rates market has shown signs of stabilization over the past week or so, and the rise in implied yields on medium-term contracts has allowed the curve to normalize following an inversion that has been observed through most of the period since mid-March." "The next ECB decision is scheduled for July 23 and markets are expecting no policy change while pricing in a 50% chance of a 25bpt hike for September 10." "Bearish/neutral – the recovery in the RSI is notable, climbing from a late June sub-30 (deeply oversold) low to the low 40s with a gentle drift back toward the neutral threshold at 50. The medium-term trend remains largely neutral, with a flat range from mid-2025 roughly bound between 1.1300 and 1.2100. We see near-term support at 1.1380 and resistance above 1.1480." (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 2:33PM EST |

|

|

| | The Australian Dollar (AUD) is confronting a notable shift in market momentum as fresh domestic data points to cooling inflation. While the currency recently experienced a sharp surge, a consecutive monthly decline in a key consumer price gauge suggests that a broader disinflationary trend is becoming firmly established. This macro shift has thrown a wrench into hawkish market expectations for additional interest rate hikes by the Reserve Bank of Australia (RBA), prompting major financial institutions to project a period of consolidation and downside vulnerability for the AUD/USD currency cross.  AUD/USD daily chart. Source: FXStreet. AUD/USD daily chart. Source: FXStreet.Established disinflation chips away at hawkish RBA betsMacro strategists at BNY highlight that price pressures in Australia are easing, led by a drop in global fuel costs. The Melbourne Institute inflation gauge fell for a second consecutive month in June, with both headline and underlying trimmed mean figures pulling back significantly. This suggests that the central bank may abandon its hawkish-leaning policy stance. The snapshot points to broader easing in both headline and underlying price pressure, suggesting disinflation is becoming more established. That could force the RBA to shift away from its neutral stance, with market pricing of 35bp of tightening by year-end now looking increasingly vulnerable if softer inflation momentum persists.

Technical fatigue sets in for the Australian Dollar after recent gainsThe strategy team at UOB observes that the Australian Dollar's previous bullish momentum has effectively run out of steam. Following a sharp multi-day rally, the AUD/USD pair has entered a minor holding pattern, with technical indicators flagging an early accumulation of downward bias that will likely cap near-term recovery efforts. Despite the relatively quiet price action, there has been a tentative build-up in downward momentum. Today, the bias for AUD is tilted to the downside, but given the lacklustre momentum, any decline is likely limited to a test of 0.6910.

Banks anticipate downward-biased near-term trajectory for the Australian DollarThe banks anticipate a cooling near-term trajectory for the Australian Dollar, indicating that its recent upward run has likely run its course. BNY indicates that if the softer domestic inflation momentum continues to chip away at the 35 basis points of priced-in RBA tightening, the currency's yield advantage will quickly erode. Mirroring this cautious macro view, UOB projects an initial multi-week consolidation phase where the AUD/USD pair remains bound between 0.6870 and 0.6980, but remains structurally bearish over a longer one-to-three-month horizon, warning that a technical breakdown could eventually drag the asset down to major downside targets at 0.6835 and 0.6707. (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 2:21PM EST |

|

|

| | TD Securities projects US output growth to move sideways in 2026, slightly below trend, with Real Gross Domestic Product (GDP) at 2.0% Q4/Q4 and unemployment around 4.3%. The Iran conflict and an oil shock pose stagflationary risks, while AI and high-income consumers support demand. Core Consumer Price Index (CPI) is seen peaking near 3.0% year-on-year in Q4 2026, with disinflation resuming in 2027. Sideways growth with stagflation risks"We expect output growth to move sideways this year, reflecting the lingering impact of the oil shock. The Iran conflict presents stagflationary risks, which we expect will keep the Fed on hold for the entire year. AI and high-income consumers have supported underlying growth." "GDP growth will likely remain slightly below trend in 2026, ending with 2.0% Q4/Q4. Stable growth should result in a still-low unemployment rate of 4.3% by Q4 2026. The labor market has signaled stabilization, and while we expect that to continue, rising input costs from the oil shock create further uncertainty that could weigh on hiring. We assign 25% odds to a US recession over the next year." "With supply chains stressed, we do not see substantial disinflation as feasible this year. We expect core CPI inflation to peak at 3.0% y/y in Q4 2026, ending the year higher than it started. The numbers are similarly high in core PCE terms. Most of the impact of higher oil prices will filter into headline inflation. We look for gradual disinflation to resume in 2027." "The outlook will be fluid amid uncertainty around developments in Iran and the Trump administration's execution of new trade, fiscal, regulatory, and immigration policies. New developments in financial markets and further escalation of geopolitical conflicts remain key risks for our economic projections over the forecast horizon." (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 2:19PM EST |

|

|

| | Commerzbank’s Dr. Marco Wagner notes that German manufacturing orders rose 1.9% in May, or 1.0% excluding large orders, pointing to an upward trend. He argues this supports a moderate recovery in German industry and a slight recovery in the broader German economy after a likely small Q2 decline. For 2026, Commerzbank maintains a 0.6% growth forecast. Orders signal modest industrial upturn"Business is gradually picking up again in terms of new orders. These rose by a surprisingly strong 1.9% in May; even excluding large orders, which are prone to fluctuations, the increase was 1%. Based on this upward trend in orders, we expect a recovery in German industry, even if it is likely to be moderate." "Seasonally and calendar-adjusted order intake in the manufacturing sector rose by 1.9% in May compared with April. Economists surveyed in advance had expected an increase of just over 1%. Excluding large orders, which typically fluctuate widely, the increase was 1.0%." "Overall, today’s figures offer hope for a moderate recovery in German industry, which—after a long period of stagnation—had recently been further battered by the war in Iran." "These are certainly all positive developments for German industry. However, we do not expect a strong recovery." "All in all, we expect a slight recovery for the German economy after it likely recorded a small decline in the second quarter. For 2026 as a whole, we continue to expect growth of 0.6%." (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 2:06PM EST |

|

|

| | - ISM Services PMI recedes to 54 in June, matching consensus.

- The US Dollar trades with decent gains on Monday.

Economic activity in the US service sector lost some momentum in June, with the ISM Services PMI easing to 54.0 from 54.5 in the previous month, matching analysts' expectations. Further poll results found that the Prices Paid Index, a crucial barometer of inflation, cooled to 67.7 from 71.3, while the Employment Index rose to 51.2 from 47.9, indicating a modest improvement in labour market conditions in the service sector. Finally, the New Orders Index weakened to 55.1 from 57.3. Market reactionThe Greenback starts the week in a positive mood, sending the US Dollar Index (DXY) back above the 101.00 hurdle.

GDP FAQs

A country’s Gross Domestic Product (GDP) measures the rate of growth of its economy over a given period of time, usually a quarter. The most reliable figures are those that compare GDP to the previous quarter e.g Q2 of 2023 vs Q1 of 2023, or to the same period in the previous year, e.g Q2 of 2023 vs Q2 of 2022.

Annualized quarterly GDP figures extrapolate the growth rate of the quarter as if it were constant for the rest of the year. These can be misleading, however, if temporary shocks impact growth in one quarter but are unlikely to last all year – such as happened in the first quarter of 2020 at the outbreak of the covid pandemic, when growth plummeted.

A higher GDP result is generally positive for a nation’s currency as it reflects a growing economy, which is more likely to produce goods and services that can be exported, as well as attracting higher foreign investment. By the same token, when GDP falls it is usually negative for the currency.

When an economy grows people tend to spend more, which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation with the side effect of attracting more capital inflows from global investors, thus helping the local currency appreciate.

When an economy grows and GDP is rising, people tend to spend more which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold versus placing the money in a cash deposit account. Therefore, a higher GDP growth rate is usually a bearish factor for Gold price.

|

|

|

| | Jul 6 2026 2:02PM EST |

|

|

| | Jul 6 2026 2:00PM EST |

|

|

| | Jul 6 2026 2:00PM EST |

|

|

| | Jul 6 2026 2:00PM EST |

|

|

| | Jul 6 2026 2:00PM EST |

|

|

| | Scotiabank strategists Shaun Osborne and Eric Theoret describe USD/CAD around 1.4215 as consolidating, with the Canadian Dollar retaining a soft undertone despite narrower US–Canada front-end spreads. They note United States-Mexico-Canada Agreement (USMCA) non-renewal prolongs trade uncertainty, while the Bank of Canada's (BoC) Q2 Business Outlook Survey may reflect this. CAD is seen as fundamentally cheap, but its undervaluation versus equilibrium has narrowed, implying limited upside potential. CAD soft as trade risks linger"The CAD retains a soft undertone. While front-end US/Canada spreads have narrowed over the past week, the CAD has been unable to pick up any ground." "Confirmation that the US would not renew the USMCA agreement was perhaps no great surprise and while there is still room for trade talks to progress, the outcome means a prolonged period of uncertainty for Canadian and Mexican exporters." "The BoC’s Q2 Business Outlook Survey this morning is likely to reflect that uncertainty to some extent at least. The CAD continues to look fundamentally cheap but the undervaluation relative to our equilibrium estimate (1.4141 this morning) has narrowed steadily over the past month which points to limited upside potential for the CAD." "But there is also the possibility that the sustained USD rally over the past six weeks is merely pausing ahead of another push higher. The 1.4250/00 range should continue to offer some resistance to a USD advance for now. Support is 1.4150 and 1.4075/80." "Neutral—USD/CAD price action is consolidating. There are some negative signs from short-term price action and the USD remains extremely overbought on the daily RSI oscillator." (This article was created with the help of an Artificial Intelligence tool and reviewed by an editor. Know more.) |

|

|

| | Jul 6 2026 1:46PM EST |

|

|

| | Jul 6 2026 1:45PM EST |

|

|

| | Jul 6 2026 1:45PM EST |

|

|

| | - GBP/JPY rises to its highest level since January 2008 as the Japanese Yen stays under pressure.

- Wide interest-rate differences continue to support carry trades and weigh on the Yen.

- Traders remain alert for possible intervention from Japanese authorities.

GBP/JPY edges higher on Monday, climbing to levels last seen in January 2008 as the Japanese Yen (JPY) remains under pressure across the board. The Yen resumed its decline after a brief pullback last week, with USD/JPY climbing back to its highest level in four decades. At the time of writing, the cross is trading around 216.75, up 0.60% on the day. The persistent weakness in the Yen is keeping traders alert to the risk of foreign exchange intervention, with Japanese officials repeatedly stating they stand ready to act against excessive currency moves if necessary. The Yen's recent weakness increasingly appears to be driven by crowded speculative bets. However, structural headwinds remain, including plans by Japan's Prime Minister to increase government spending, which could worsen the fiscal outlook at a time when the country's debt-to-GDP ratio is already above 250%. The Bank of Japan (BoJ) ended more than a decade of ultra-loose monetary policy in March 2024 and has gradually raised interest rates since then, lifting its policy rate to 1.0% from 0.75% at its June meeting, the highest level since 1995. Even so, the pace of policy normalization remains slow, leaving Japan's interest rates well below those of other major economies. The wide interest-rate differential continues to weigh on the Yen by encouraging carry trades, in which investors borrow at Japan's relatively low borrowing costs to invest in higher-yielding currencies such as the British Pound (GBP). Meanwhile, the BOJ's hawkish stance has lifted Japanese Government Bond (JGB) yields, but the move has failed to support the Yen because higher yields also raise future debt-servicing costs. The benchmark 10-year JGB yield climbed to 2.83% on Monday, its highest level since May 1997. With the UK and Japan economic calendars relatively light this week, traders are likely to keep a close eye on any signs of foreign exchange intervention from Japanese authorities.

Japanese Yen Price Today

The table below shows the percentage change of Japanese Yen (JPY) against listed major currencies today. Japanese Yen was the strongest against the New Zealand Dollar.

|

USD |

EUR |

GBP |

JPY |

CAD |

AUD |

NZD |

CHF |

| USD |

|

0.16% |

0.01% |

0.62% |

0.15% |

0.09% |

0.48% |

0.35% |

| EUR |

-0.16% |

|

-0.13% |

0.44% |

-0.00% |

-0.04% |

0.33% |

0.19% |

| GBP |

-0.01% |

0.13% |

|

0.59% |

0.11% |

0.04% |

0.47% |

0.35% |

| JPY |

-0.62% |

-0.44% |

-0.59% |

|

-0.47% |

-0.52% |

-0.15% |

-0.20% |

| CAD |

-0.15% |

0.00% |

-0.11% |

0.47% |

|

-0.08% |

0.33% |

0.22% |

| AUD |

-0.09% |

0.04% |

-0.04% |

0.52% |

0.08% |

|

0.41% |

0.29% |

| NZD |

-0.48% |

-0.33% |

-0.47% |

0.15% |

-0.33% |

-0.41% |

|

-0.13% |

| CHF |

-0.35% |

-0.19% |

-0.35% |

0.20% |

-0.22% |

-0.29% |

0.13% |

|

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Japanese Yen from the left column and move along the horizontal line to the US Dollar, the percentage change displayed in the box will represent JPY (base)/USD (quote).

|

|

|

| | Jul 6 2026 1:44PM EST |

|

|